Fraud and forgery have turned refinance transactions into the mortgage industry’s most dangerous minefield. The numbers are staggering — and the implications for every Notary Signing Agent in America are urgent.

For years in the mortgage finance industry, there has been a general perception of refinance transactions that goes something like this: Refinance transactions are low-risk. The borrower already owns the home. The title is clean. What could go wrong?

As it turns out, quite a bit.

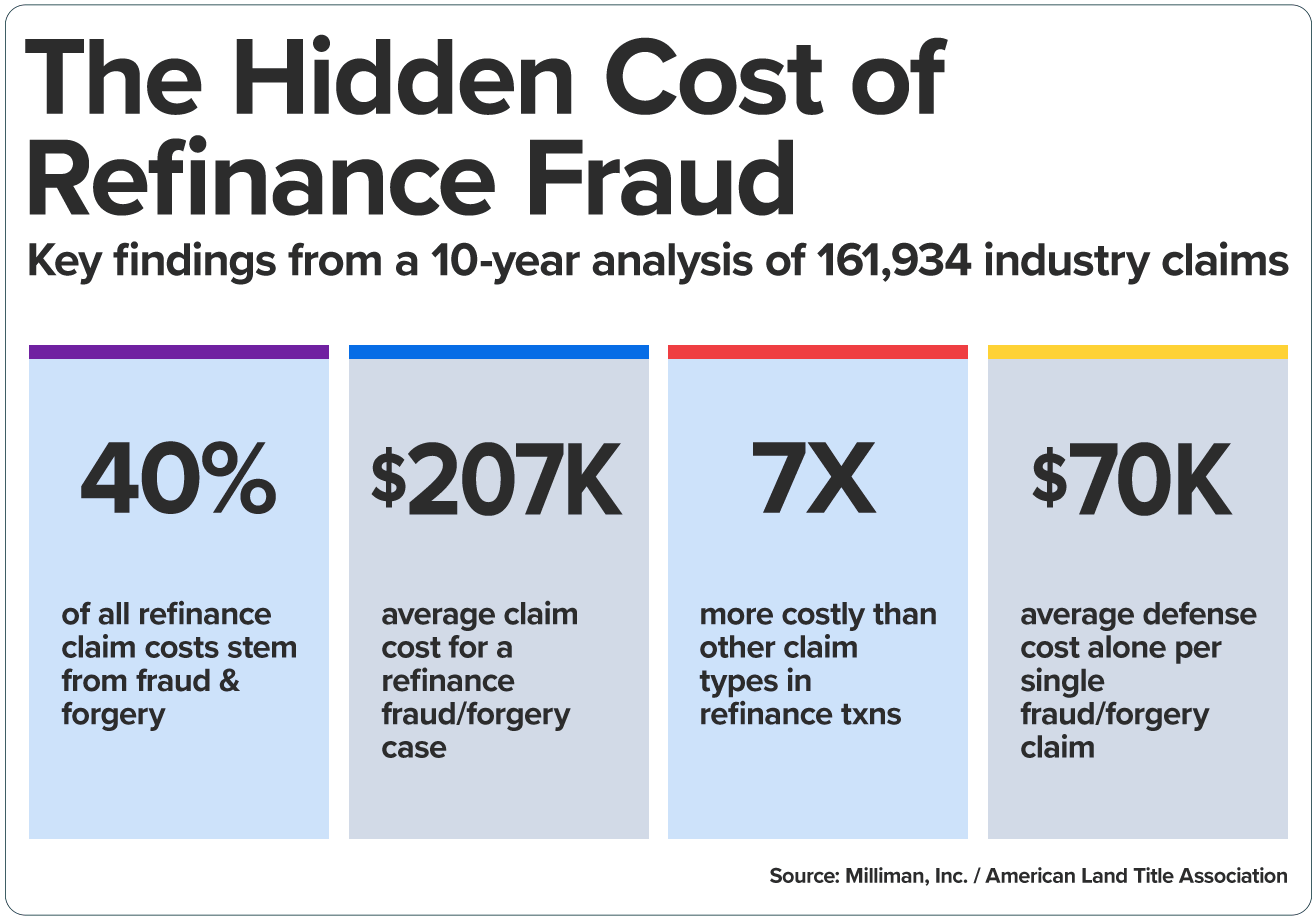

A comprehensive analysis recently released by Milliman, Inc. and commissioned by the American Land Title Association (ALTA), examined more than 161,000 title insurance claims over a decade and arrived at a conclusion that should resonate with every Notary:

“Both refinance transactions and lenders are exposed to significant losses, with historical data indicating that average claim severity is higher for refinances than for purchases. The largest losses are typically associated with fraud and forgery, which cannot be easily identified through a search of public records.”

In simpler terms, refinances are more vulnerable to fraud than we realize. The kind of fraud that can’t be caught by a records search. The kind that can only be stopped by a trained, vigilant professional who is physically present when documents are signed.

That professional is you. Notaries are the last line of defense against the growing problem of refinance fraud.

How widespread is the problem of refinance fraud?

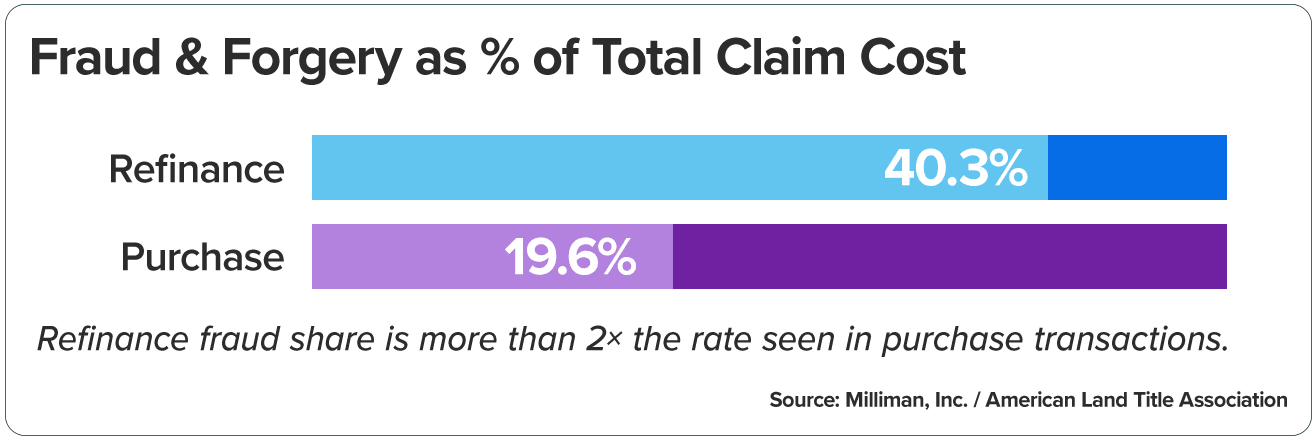

The data quantifies just how severe the issue has become. Fraud and forgery claims account for approximately 40 percent of the total title insurance claim cost associated with refinance transactions. That figure is more than double the rate seen in purchase transactions, where fraud and forgery represent 20 percent of total claim costs.

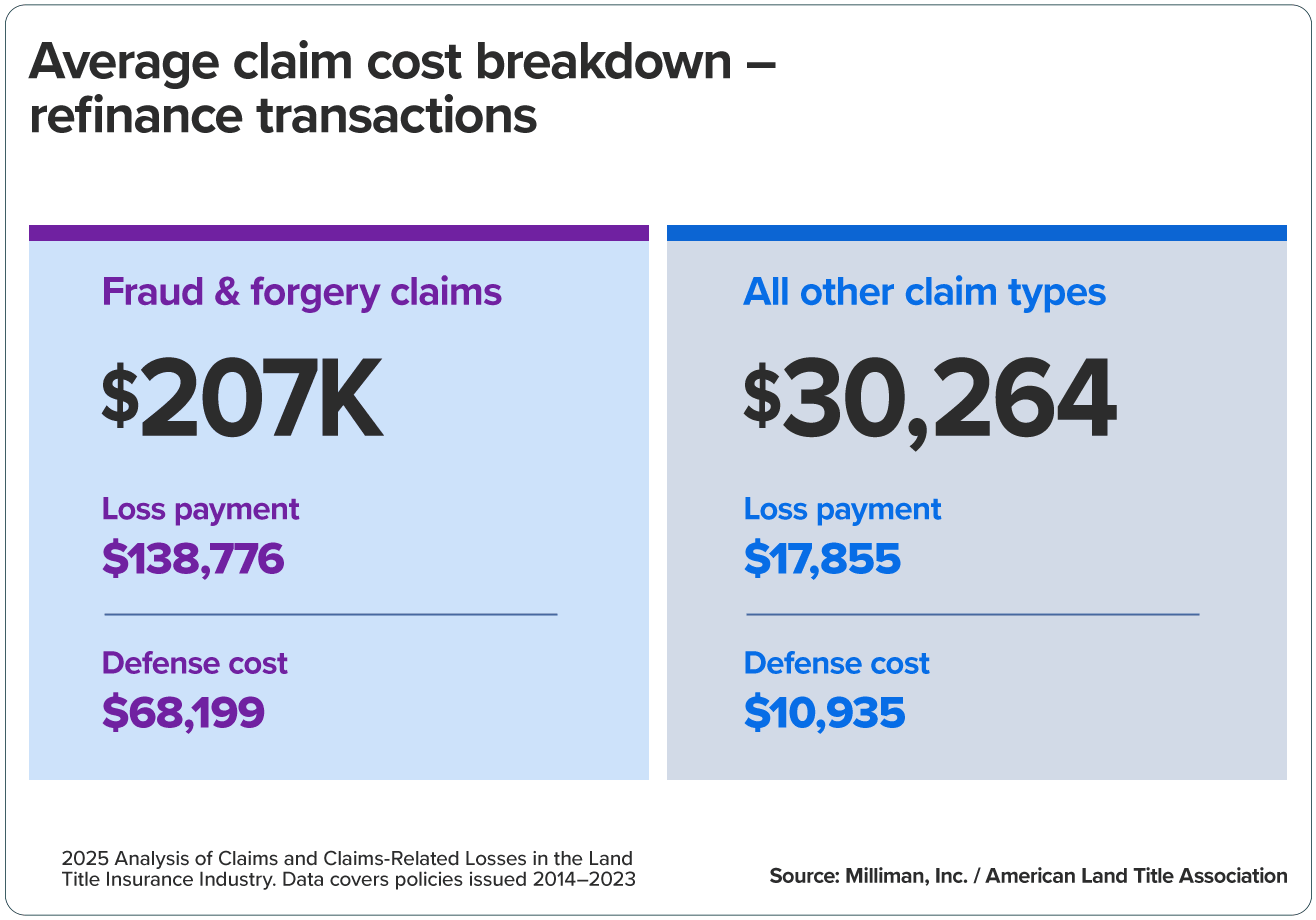

Even more sobering: The average cost of fighting refinance fraud in court runs about $207,000 — including loss payments and defense costs. That’s nearly seven times higher than the average cost for all other claim types, which average about $30,000.

And critically, approximately 40 percent of all refinance losses and expenses are linked to fraud and forgery issues that cannot be identified through public record searches. No title search can catch a criminal impersonating a homeowner. No database query can flag a synthetic identity assembled using AI-generated documents.

How do Notaries prevent refinance fraud?

One of the best ways to catch these schemes is a Notary doing their duty — carefully, methodically, and without shortcuts.

“Notaries play an important role in preventing real property document fraud,” said Brooke Merritt, the NNA’s Director of Government & Policy Planning. “A diligent, well-trained Notary exercising a high degree of care is a strong safeguard against harm, providing the human judgment needed to catch red flags that technology and data tools can’t always detect.”

Real-life cases of refinance fraud

The data points to a national crisis, but some of the most vivid illustrations of mortgage fraud come from court documents, E&O insurance claim reports, and local news reports.

While the following examples are not all related to refinance fraud, they demonstrate the methods criminals use to fool the system, how diligent Notaries helped prevent some cases, and how Notary mistakes or carelessness made things worse in others.

- A Charlotte, North Carolina, man was stunned when he learned he was the victim of seller impersonation fraud. An imposter tried to refinance his home — a home he had already paid off — after obtaining his personal information, including his driver’s license. The cash-out refinance would have netted the fraudulent actor about $450,000. The fraud was caught when an attorney and his paralegal Notary visited the victim’s residence to verify his identity in person, and they discovered the impersonation.

- A Notary authorized to perform remote online notarizations completed a signing that turned out to be fraudulent. The video recording of the transaction indicated that the Notary did not follow proper procedures by failing to examine the signer’s ID documents properly and permitting a second person in the room to assist the signer with the knowledge-based authentication questions. The case landed in court, and the Notary incurred $75,000 in settlement and legal fees, which were paid out of her $100,000 E&O policy.

- A Notary was accused of notarizing a warranty deed fraudulently, though she had never met the signer and had no record of the signing. Later, it came to light that the seal was forged and did not match the Notary’s official seal. She promptly reported it to the police and was cleared of wrongdoing, but her E&O policy was hit for $14,000 in attorney and legal fees from her $25,000 limit.

- Federal prosecutors are currently investigating a Southern California real estate broker in a $1.5 million case that demonstrates how seller impersonation can slip past lenders, title companies and Notaries. According to a federal criminal complaint, a group of fraudsters allegedly used the stolen identities of the true homeowner and a purported buyer to push through a fraudulent sale, securing about $975,000 in loan proceeds. The case remains under investigation.

- Bonus Example: If you haven’t read about the ‘Graceland’ case, check it out here.

How AI and synthetic identity fraud make the Notary’s job more difficult

If the ALTA/Milliman data describes an emerging pattern, the threat environment that Notaries are navigating today has grown considerably more complex.

Synthetic identity fraud — in which criminals use AI tools to combine real and fabricated information to create convincing counterfeit identities and documents — has become one of the fastest-growing categories of financial crime. AI-generated ID documents can now reproduce security features that previously served as reliable fraud detection checkpoints. A driver’s license that would have looked obviously fake five years ago may today be nearly indistinguishable from a genuine document to the casual eye.

Seller impersonation fraud has also spiked dramatically, with criminals targeting vacant land and debt-free properties specifically because those transactions are less likely to involve lenders with robust verification systems — and more likely to flow through a signing table without a second look.

This is precisely why Notaries are more important than ever to prevent fraud.

The shift toward AI-enhanced fraud doesn’t diminish the value of the human expert in the room — it magnifies it. Sophisticated software can be fooled by sophisticated forgeries. A trained, engaged Notary who asks the right questions, examines ID documents carefully, and trusts their instincts when something feels wrong is still the mechanism the system depends on most.

What Notaries need to watch for at the signing table to stop fraud

The NNA’s educational resources at NationalNotary.org offer a robust framework for Notaries navigating high-risk transactions.

Common warning signs at the signing table include:

- Requests by signers to avoid personal appearance before the Notary.

- Presentation of fake IDs, or stolen IDs from other individuals.

- Signers who can’t answer questions about their identity.

- Parties who pressure another person to sign, or fail to have awareness of what they are signing.

If property deeds or financial powers of attorney are part of the closing package, especially if the signers are elderly. Each of these scenarios calls for a specific, practiced response from Notaries: slow down, verify identity, and never allow urgency — from any party — to compromise you from following proper notarization procedures. Your role as a Notary is not merely ceremonial. If you do your job correctly, you become one of the most powerful fraud prevention tools in the entire transaction chain.

For refinance fraud specifically, certain warning signs of possible fraud occur regularly, according to the study:

- A signer who seems confused about the property they supposedly own.

- A “borrower” who can’t describe their own address when asked a simple, neutral question.

- Pre-signed documents — a serious red flag, since in most cases the Notary personally brings the documents from the lender for the borrower to sign.

- A third party who controls the flow of the appointment and answers questions before the signer can.

- Pressure to skip standard ID verification for the sake of speed.

- A signer pushing you to urgently notarize a document without common standards of care.

- And increasingly, ID documents that pass a cursory glance but fail closer examination — slightly off fonts, edges that look digitally altered, security features that don't quite hold up.

Cash-out refinances on debt-free properties deserve particular scrutiny. As the North Carolina case described earlier illustrates, a paid-off home represents exactly the kind of target that organized fraud rings seek out — a property with substantial equity, no lender in the loop, and proceeds that will flow directly to whoever walks away from the closing table as the “borrower.”

Important takeaways for Notaries involved in refinance transactions

The ALTA/Milliman report is a document that the entire mortgage industry should study. For Notaries, it provides something even more specific: evidence, in the form of hard statistical data, that the work you do at the signing table carries enormous financial and human consequences.

The fraud landscape is evolving. AI tools are lowering the barrier to sophisticated identity crimes. Seller impersonation rings are growing more organized and ambitious. And refinance transactions — long assumed to be the safer, simpler side of the mortgage business — have emerged as the highest-severity category of title insurance loss in the industry.

Notaries are more important than ever. The data confirms it. The headlines confirm it. And every signing table you walk up to — with your ID credential technology, your journal, your training, and your judgment — is a small piece of the line that holds.

Frequently asked questions

Why are refinance transactions considered high risk for fraud?

Refinance transactions are increasingly high risk because they often involve properties with significant equity and fewer verification checkpoints. According to data from the American Land Title Association, fraud and forgery account for about 40% of total title insurance claim costs in refinances — double the rate seen in purchase transactions.

Why are Notaries critical in preventing refinance fraud?

Notaries serve as the final checkpoint in the transaction. They verify signer identity, witness signatures, and ensure proper procedures are followed. Because they interact directly with the signer, Notaries are uniquely positioned to detect red flags that automated systems and document reviews cannot catch.

How do Notaries help prevent mortgage and refinance fraud?

Notaries help prevent fraud by:

- Verifying government-issued identification

- Ensuring the signer personally appears

- Refusing to notarize incomplete or suspicious documents

- Maintaining detailed journal records of the signing

For additional guidance on fraud prevention in mortgage signings, visit the NNA’s Knowledge Center and The National Notary Bulletin news blog at NationalNotary.org.

Phillip Browne is Vice President of Communications at the National Notary Association.